All guarantees are subject to the claims-paying ability and financial strength of the issuing insurance company.

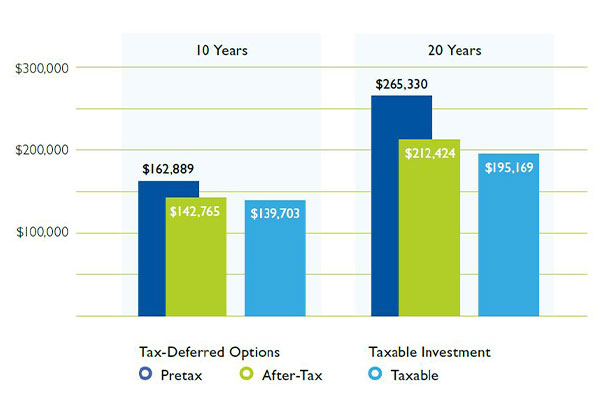

Tax-deferral assumptions: Hypothetical example for illustrative purposes only. Assumes a nonqualified contract with a cost basis of $100,000. The full amount after 20 years before taxes equals the purchase payments plus interest, $265,330. The amount withdrawn after taxes are paid is calculated by taking the full amount and subtracting the cost basis; it is then multiplied by 0.68 (32% ordinary income-tax rate) and adding back in the cost basis, for a total of $212,424 after taxes.

Actual tax rates may vary for different taxpayers and assets from those illustrated (for example, capital gains and qualified dividend income). Actual performance of your investment will also vary. Lower maximum tax rates on capital gains and dividends would make the investment return for the taxable investment more favorable, thereby reducing the difference in performance between the examples shown. Consider your personal investment time horizon and income-tax brackets, both current and anticipated, when making an investment decision. Hypothetical returns are not guaranteed and do not represent performance of any particular investment. If annuity charges were included (withdrawal charges or optional benefit fees), the tax-deferred performance would be significantly lower.

Annuity withdrawals and other distributions of taxable amounts, including death benefit payouts, will be subject to ordinary income tax. For nonqualified contracts, an additional 3.8% federal tax may apply on net investment income. If withdrawals and other distributions are taken prior to age 59½, an additional 10% federal tax may apply. A withdrawal charge and a market value adjustment (MVA) also may apply. Withdrawals will reduce the contract value and the value of the death benefits, and also may reduce the value of any optional benefits.

Under current law, a nonqualified annuity that is owned by an individual is generally entitled to tax deferral. IRAs and qualified plans, such as 401(k)s and 403(b)s, are already tax deferred. Therefore, a deferred annuity should be used only to fund an IRA or qualified plan to benefit from annuity other features other than tax deferral. These include lifetime income and death benefit options.

A fixed indexed annuity is not a security and does not participate directly in the stock market or any index, so it is not an investment.

The “S&P 500®” index is a product of S&P Dow Jones Indices LLC, a division of S&P Global, or its affiliates (“SPDJI”), and has been licensed for use by Pacific Life Insurance Company. Standard & Poor’s® and S&P 500® are registered trademarks of Standard & Poor's Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Pacific Life’s product is not sponsored, endorsed, sold, or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500® index.

The index is not available for direct investment, and index performance does not include the reinvestment of dividends.

Pacific Life, its distributors, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should see advice based on the taxpayer's particular circumstances from an independent tax advisor or attorney.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Pacific Life Insurance Company (Newport Beach, CA) is licensed to issue products in all states except New York. Product availability and features may vary by state. Fixed annuity products are available through licensed third parties.

No bank guarantee • Not a deposit • Not FDIC/NCUA insured • May lose value • Not insured by any federal government agency

")